IRGA and 27 Advisory Consolidate to Deliver Plantation Transformation Services to Clients in the Agricultural Sector

08/09/2023

MPOA National Palm Oil Conference (NPOC) 2023

26/10/2023

The Malaysian Palm Oil Industry and EUDR Compliance

On 29th of June 2023, the newly-minted European Union’s Deforestation Regulation (EUDR) policy came into force: “The main goal of the EU Deforestation-free Regulation is to ensure that the production of certain goods and commodities will not contribute to further degradation of forest ecosystems. This is also expected to reduce emissions of greenhouse gases and conserve biodiversity.” This policy applies to 7 groups of commodities entering the 27 member states of the EU and is expected to take effect end-2024.

The implications of this new regulatory policy and why it is plunging many agricultural commodity markets into a tailspin is expanded upon here

The Regulation - The Reaction

This new regulatory policy has impacted various agricultural commodity markets worldwide and has become the contentious issue currently being debated in the plantation sectors in Malaysia and Indonesia – the world’s two largest producers of palm oil. Apart from palm oil, the EUDR policy also addresses the expansion of agricultural land linked to cattle farming (beef), production of timber, soy, coffee, cocoa and rubber, as well as their related products including leather, chocolate, rubber tyres and furniture.

The policy outlines the obligation of these industries to conduct extensive due diligence on their value chain - (with extensive, land traceability studies and more) - to ensure that the goods are not linked in any way to deforestation, forest degradation, human rights and other associated legal or social infringements on land occurring post 31st December 2020.

On 29th of June 2023, the producing countries reacted collectively, voicing their concerns in a joint letter signed by their ambassadors in Brussels. Apart from Malaysia and Indonesia (the main palm oil producing countries) the other signatories were Argentina, Brazil, Bolivia, Colombia, Ecuador, the Dominican Republic, Ghana, Guatemala, Honduras, Ivory Coast, Mexico, Nigeria, Paraguay, Peru and Thailand.

EUDR Due Diligence Framework Requirements

The due diligence system and its questionably short, implementation timeline involves three parts:-

- Information gathering – Collecting data on your product´s supply chain, including the geo-localisation and time period of primary production.

- Risk assessment – Assessment of the information to determine the risk of deforestation, forest degradation and illegality associated with the product.

- Risk mitigation – Actions to reduce non-negligible risks to negligible levels. Actions include requesting further information, independent surveys, scientific product testing or audits.

Additionally, the companies or traders must submit these results to their designated national regulatory authority, to show compliance with the standards set out under the EUDR. Countries are then allocated a ‘low risk’, ‘medium risk’ or ‘high risk’ ranking based on the data submitted through these methods.

Then, operators and traders in the EU will, in turn, be required to implement due diligence on their supply chains to ensure that they are not linked to deforestation or forest degradation activities occurring on land post 31st December 2020.

Concerns regarding the EUDR vs current Mandatory Self-Policing Regulations in Malaysia

The issue has become a contentious one in that most countries consider the policy to be overly strict in terms of what constitutes actual deforestation and legal infringements, as well as the unrealistically, short timeline given to companies to implement these required changes. Furthermore, the EU’s disregard for the stringent, self-policing of existing Palm Oil companies’ certification and initiatives by regulatory bodies (like MPOB, MSPO, RSPO and ISCC) have not gone down well in Malaysia. This is especially so when 96% of Malaysian plantation companies have been adopting the government mandated Malaysian Sustainable Palm Oil (MSPO) standard for their exports to EU-27 in 2022 and have been 95% certified sustainable under either MSPO, RSPO or ISCC platforms, ensuring stringent compliance with ESG standards. The export to EU-27 last year consisted of 1.6 million tonnes of palm oil and palm oil derivative products.

As far as due diligence goes, a recent study by World Resources Institute (WRI), ranked Malaysia among the top 5 countries globally for reducing deforestation, whereby primary forest loss is reported to have reduced by a whopping 57%. It has also seen a reduction of 180,000 hectares in oil palm planted land since 2020. Similarly, other commodities that recorded steep reductions in planted area between 2021 and 2022 are;-

- cocoa from 3.9 million hectares in 1991 to less than 6,000 hectares in 2022

- rubber (49% reduction) from 1.8 million hectares in 1991 to only 1.1 million hectares in 2022

- licensed timber concessions for harvesting reduced from 370,000 hectares in 2017 to 154,000 hectares in 2021

Malaysia’s forest cover currently stands at 54.5% or 18 million hectares.

EUDR Risk Assessment

To add to this unprecedented ruling, the issue of determining the risk category will require the producing countries to spend time and resources to try and influence the benchmarking of risks of exports to EU-27, categorised as Low Risk – 1%, Standard Risk – 3% and High Risk – 9%.

To elaborate on this, the regulation will set up a new monitoring system to ensure risk compliance. It will audit producing countries, within and without the EU, depending on the estimated risk of forest loss or degradation. For example, in countries deemed “high risk”, authorities will carry out checks on 9% of a sector’s traders and operators. For countries deemed “standard risk” or “low risk”, monitoring will involve 3% and 1% of the operators respectively.

It certainly looks like it is going to be a challenging exercise moving forward in terms of navigating the various procedural and operational hurdles put forward by the EUDR framework, notwithstanding the associated increases that compliance will bring to the industry’s production costs.

Therefore, a satisfactory compromise will have to be navigated with the EU-27 to ensure that while factors contributing to global and planetary climate change are addressed, it does not jeopardise the national socio-economic framework of the Malaysian palm oil industry.

The Plight of the Smallholders in Malaysia and Indonesia

Although many welcome the EU’s new regulation for deforestation-free commodities, the concerns over the impact on small-scale farmers has been grossly overlooked. The EU’s unprecedented action to eliminate deforestation from its supply chains fails to consider the poorest growers that form the backbone of palm oil production in Southeast Asia. This oversight could cost developing countries dearly and ultimately risk thwarting the bloc’s plan to protect the world’s forests.

The issue of deforestation within the industry has been a noted concern over the past 30 years, however it has generally fallen into the purview of bilateral trade agreements between countries. In recent times, the government has allowed the private sector to voice their opinion on what ought to be defined as “sustainable production” and the EUDR now represents the first instance in which the matter has taken the form of a global trade concern.

An estimated 7 million smallholders and small farmers are dependent on oil palm cultivation for a living. Ignoring the smallholders would be socially and economically impactful. Smallholder production areas constitute approximately 30% of the total cultivated landbank in Malaysia and about 40% in Indonesia. Their exclusion from the supply chain would therefore have a drastic effect both within the local industry and in international markets.

A key challenge that this group faces lies in effectively demonstrating the traceability of their palm oil products, as the EUDR policy requires that plantation operators produce detailed year-of-planting records as well as satellite imagery showing that the designated planted area is free from deforestation activities.

The New Due Diligence Challenge

With respect to the geolocation requirements, companies are required to produce the following information. Firstly, they must show where their palm oil FFB originated from, secondly, who are the owners of the land in question, and finally, they must supply the information showing the area is deforestation-free.

To provide an illustration of the complexity involved in demonstrating this information, one can consider the instance of the Indonesian-based oil palm company Golden Agri-Resources, which controls 582,633 hectares of land used for oil palm.

The company produces 25% of its palm oil on its own plantations, with 75% coming from third parties. According to data submitted to the RSPO (Roundtable on Sustainable Palm Oil), GAR has six refineries, 49 proprietary mills and utilises 429 third-party supplier mills.

The mills which the company uses change throughout the year for various reasons, including quality control and ESG compliance issues, and when considering that an individual mill can source from thousands of smallholder operations, the gravity of the challenge involved in consistently meeting the EUDR disclosure criteria moving forward becomes more apparent. The effect of this is that companies would likely narrow their pool of suppliers, thus leaving smallholders in the lurch.

Arguments have been put forward by industry professionals to provide smallholders with support mechanisms such as access to high-quality seeds and fertilisers to increase their productivity without expanding into forested areas. Nevertheless, the EUDR criteria at present does not appear to take into considerations such challenges faced by smallholders in nations such as Malaysia, Thailand and Latin America.

EU-27 Imports Palm Oil for Energy (Biofuels)

Another point of concern is that Analysts have discovered that only 35% of palm oil imported by the EU-27 has been utilised for food and beauty products, apart from leather and rubber tyres. Instead, palm oil is used mainly for energy, with about 65% of imports going into biofuels in 2018. European lawmakers have labelled the practice unsustainable and pledged to phase out the fuel by 2030! Does this mean that we can anticipate a sharp decline in palm oil imports to EU in the coming years?

The Importance of Oil Palm Trade with European Nations

In her presentation titled “EU Deforestation Regulation : Challenges & Opportunities” at the National Palm Oil Conference (NPOC) on 2nd October 2023, Belvinder Kaur Sron, CEO, Malaysian Palm Oil Council (MPOC) discussed the reasons for why maintaining trade relation with European nations is important, irrespective of the new EUDR policy. She highlighted several key points, with the focus being that the EU remains the third largest consumer of palm oil after Indonesia and India.

Sron’s main reasons for why exports to the European Market matter were:-

- The EU represents one of the top 5 markets globally for Malaysian Palm oil

- It is the third largest consumer of Palm Oil after Indonesia and India

- Europe is a vital part of the sustainable Palm Oil movement. If sustainable Palm Oil is not available, other oils will replace the vacuum

- With MSPO, Malaysia can be a market leader when the EUDR requirements kick in from 2025 as most large companies are ready to meet the requirements

- The Brussels regulation has a global impact

The following facts were also shared:

- Malaysian and Indonesia were competing in similar markets

- A diffeentiation strategy is needed

- MSPO as an opportunity to differentiate Malaysian Palm Oil from other competitors

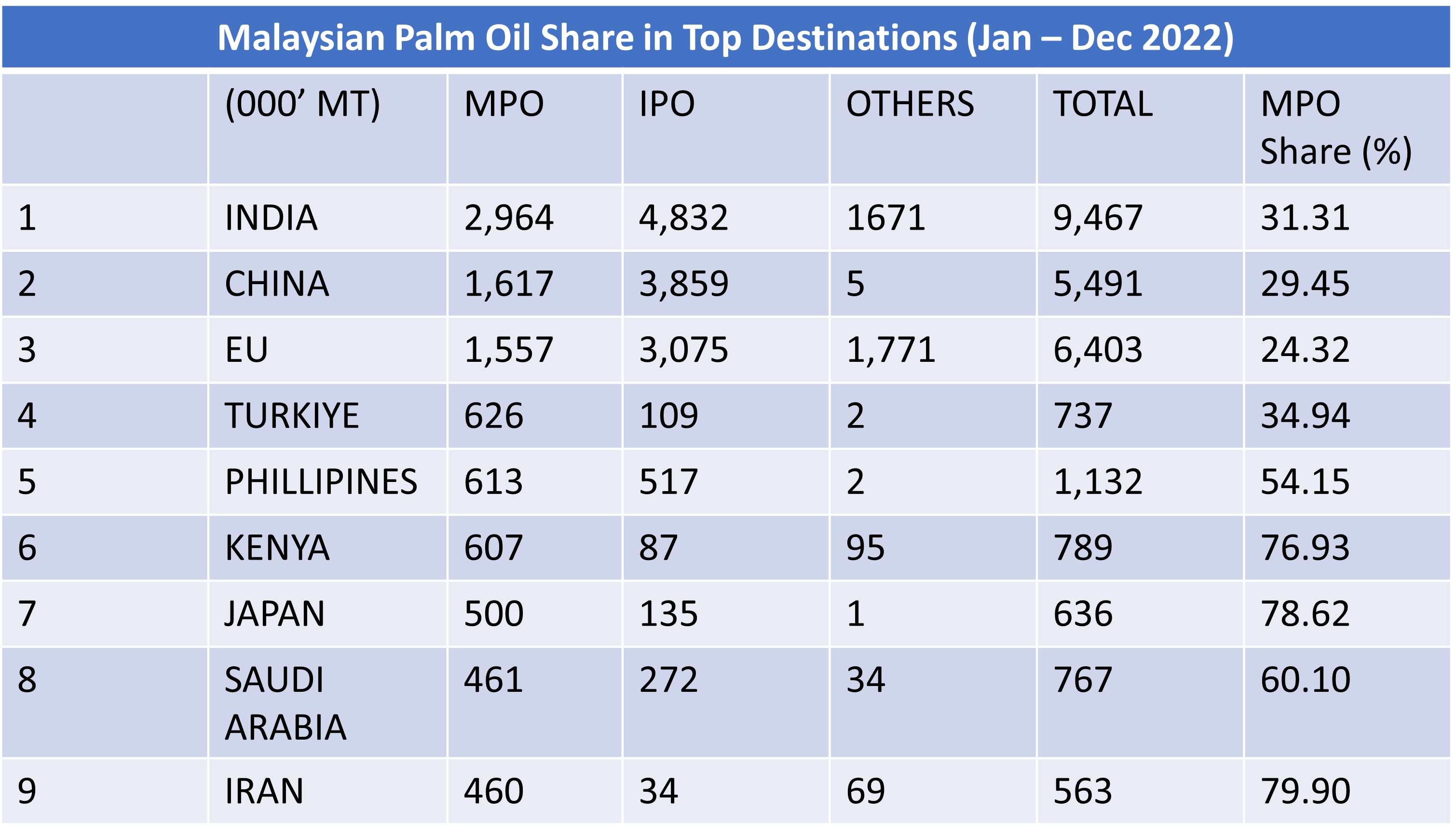

She also highlighted palm oil shares in 2022 by some of the main countries in a table:-

In closing, Sron suggested that it would be wise for the industry to consider long-term strategies to navigate the challenges that might be posed from EU market exclusion. Among those put forward included seeking new markets in developing and emerging economies that would be favourable for trade as well as increasing the uptake of palm oil within current importing countries.

Conclusion

Ultimately, it remains to be seen if the EUDR’s strict policy will in fact be realistically achievable. A general sentiment that ripples through industry channels is that it may have been wise for the EU to consult with the full range of affected stakeholders, particularly within developing nations, before setting its strenuous standards.

As oil palm producing nations continue to navigate the challenges brought about by the EUDR, it is hoped that a compromise can be reached which factors in the challenges of smallholders and developing nations, and provides the necessary support mechanisms that allow them to achieve compliance without jeapordising their economic welfare.

{kind=link}

{kind=link}

{kind=link}